OSI, PSI, the IMF and fantasy

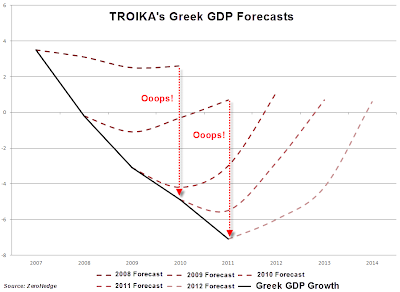

After much intense negotiation, it seems there is a new deal for Greece. Or at least that is how it has been presented in the media. But what sort of deal is it, and does it solve the Greek problem? The wording of the Eurogroup's statement does not suggest that there is a "deal", as such. All it says is that the official sector - the ECB and Eurogroup - may be prepared to accept poorer returns on their holdings of Greek debt. The specific measures that they "would consider" are the following: 1% reduction in interest rates on the loans made available under the "Greek Loan Facility" (the first bailout) 0.1% reduction in the fees paid by Greece for EFSF guarantees of its debt deferral of interest for ten years on EFSF loans (the second bailout) extension of maturities on EFSF and bilateral loans by fifteen years repatriation of interest paid by Greece to the ECB and national central banks (the "Eurosystem") These measures are condi